|

Not this time. It is remarkable that, some 18 months after peak inflation, the trend is still a good one-point to one-and-a-half-percentage-point above pre-COVID trend, in most regions.

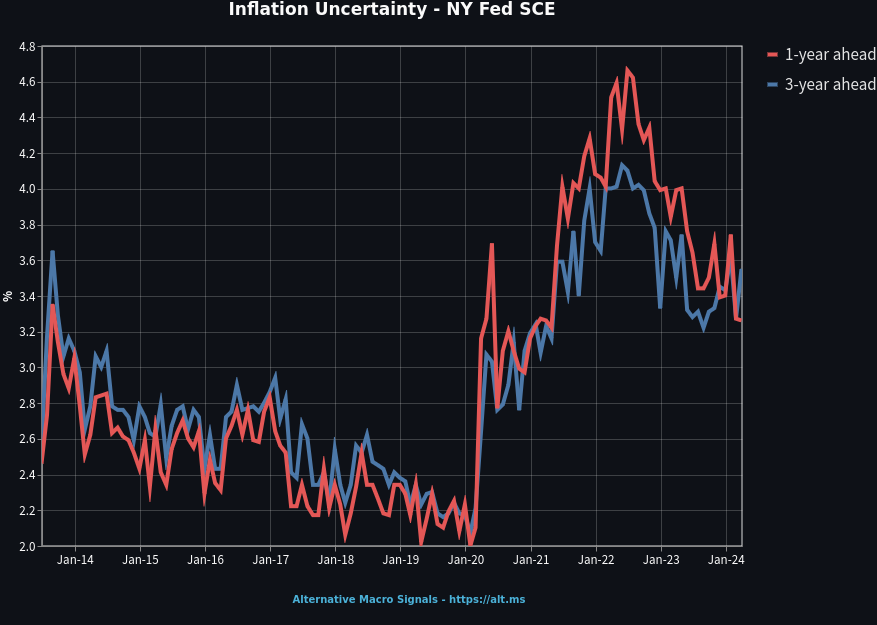

Some COVID scars may, indeed, run unusually deep. For instance, households still perceive inflation uncertainty well-above COVID levels:

The most obvious lesson from this simple observation should be that the "normalization process" is unusually long this time.

More fundamentally, it should also bring the (somewhat overlooked) question of economic volatility:

Did the "Great Moderation", the era of economic stability which started in the mid 80s, end with COVID?

If globalization and a stable (geo)political framework contributed to it, as is commonly acknowledged, then economic stability must be seriously challenged now.

Time will tell. Economists had been debating for decades on the factors behind the "Great Moderation" phenomenon.

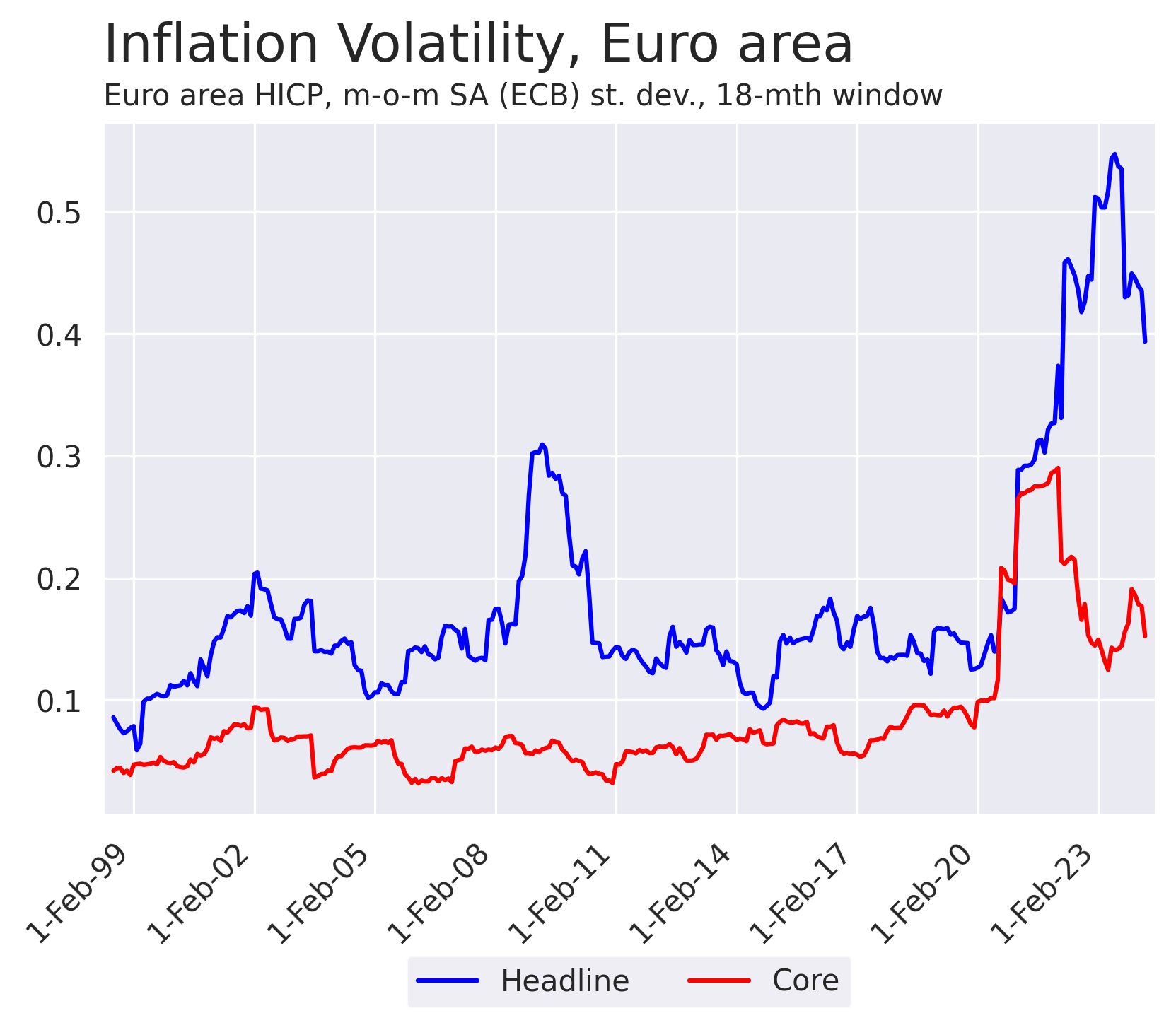

In a series on inflation dynamics post-COVID, we observe that Euro area inflation volatility is far from back to normal.

For observers, one implication of persistent inflation volatility would be to avoid jumping the gun and stay focused on near-term inflation developments, resisting perhaps the temptation to extrapolate them.

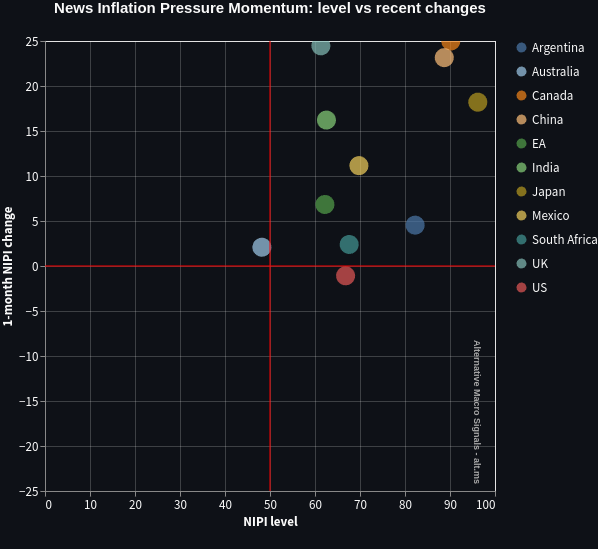

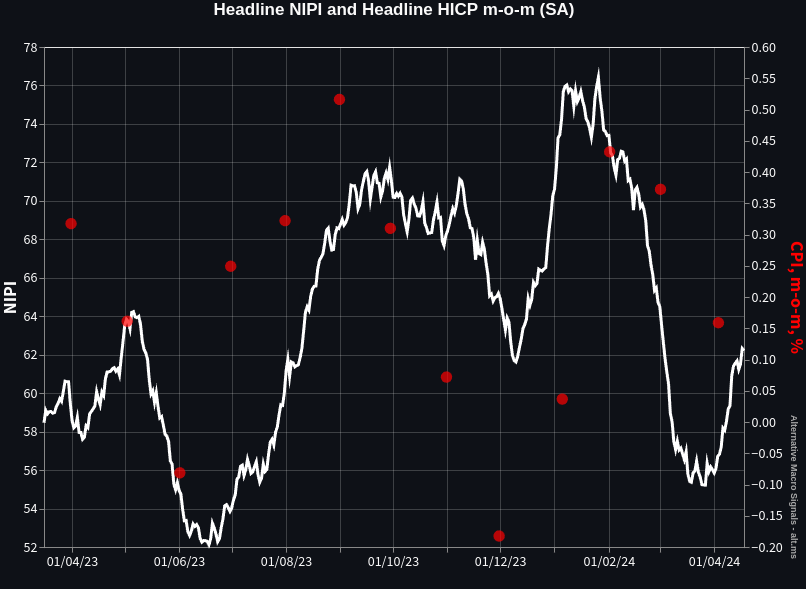

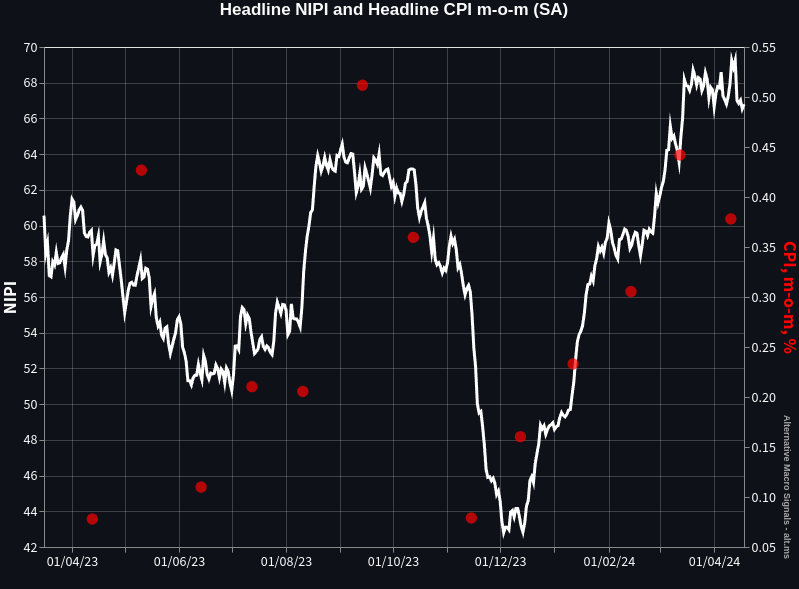

On that note, we have been observing, in our data in the last month or so, a tendency for the inflation momentum to move back to the strong-and-accelerating quadrant, out of the strong-and-decelerating one:

|